us japan tax treaty interest withholding

Japanese withholding tax rate might be reduced or exempt if. Allows for the taxation of gains from the sale of real property and real property.

2

The withholding tax exemption certificate can be issued if the income is attributable to the PE in Japan.

. There is a tax treaty between Japan and the country where the non-resident resides. Incentives Various tax credits are available including an RD credit. 3The definition of direct investments for purposes of the 10 percent withholding rate on dividends would be.

FP receives interest arising in the United States. Foreign companya resident in Dividends Interestb Royaltiesb Tax sparing relief Non-treaty nil 15 10 A Treaty Albania nil 5 0c 5 NA Australia nil 10 10 NA Austria nil 5 0c 5 NA Bahrain nil 5 0c 5 NA Bangladesh nil 10 10 A Barbados nil 12 0c 8. Continue reading Tax treaties.

For example assume that FCo a company that is a resident of Japan owns a 50 percent interest in FP a partnership that is organized in Japan. Notable changes in the protocol are enlarged exemptions of taxes required to be withheld on payments of interest and dividends. The 2013 protocol introduces a number of changes to the treaty such as a general withholding tax exemption for interest a broader.

Stay up-to-date with the latest tax news rates and commentary anytime anywhere. The main points of the amendments to the Japan-US tax treaty. Deloitte taxhand - information and insights from Deloittes tax specialists globally.

Pension funds are exempt under certain conditions. Broadens exemptions from source country withholding on most interest limits source country withholding on contingent interest to 10. Corporations for this purpose.

Japan - Tax Treaty Documents. Specifically the triggered provision concerns the rate of withholding tax imposed on certain interest payments. Reduced tax rates.

Application of tax treaty. Tax treaties increase FDI activity in USA and other developed countries. Treaty eliminates the withholding tax on royalties certain dividends and interest and generally updates the current US-Japan income tax treaty.

These changes are effective for. This result in order is only carry out more than before the other contracting state. Withholding tax should provide more flexibility in relation to treasury operations for multinational groups headquartered in the US or Japan and entitled to benefits under the Treaty subject to any other restrictions on interest deductibility under either US or Japanese domestic law eg BEAT in the former and earnings stripping in the latter.

Treatment of pass through entities. Withholding Tax Rates on Dividends and Interest under Japans Tax Treaties The list below gives general information on maximum withholding tax rates in Japan on dividends and interest under Japans tax treaties as of 12 January 2022. Accordingly with the trigger of the most favored nation clause.

While Japan ratified the protocol in the Diet on June 17 2013 ratification on the US side had been held up in the Senate which finally ratified it on July 17 2019. The income tax treaty between Chile and Japan has triggered the most favored nation clause contained in Chiles income tax treaties with Canada and Mexico. 132 Non-Resident Withholding Tax Rates for Treaty Countries1 Country2 Interest3 Dividends4 Royalties5 Pensions Annuities6 Algeria 15 15 015 1525 Argentina7 125 1015 351015 1525 Armenia 10 515 10 1525 Australia 10 515 10 1525 Austria 10 515 010 25 Azerbaijan 10 1015 510 25 Bangladesh 15 15 10 1525 Barbados 15 15 010 1525 Belgium8 10 515 010 25.

Summary of US tax treaty benefits. November 17 2021. 30 August 2019.

Japan Highlights 2020 Page 3 of 10 Participation exemption There is no participation exemption in respect of capital gains but there is a 95 foreign dividend exemption see above under Taxation of dividends. Taxation of such interest is fully realised by tax withholding so resident individuals are not required to aggregate such interest income with other income. 3 See Staff of the Joint Committee on Taxation Explanation of Proposed Income Tax Treaty Between The United States and Japan JCS-1-04 February 19 2004 at 74.

The US Japan tax treaty eliminates withholding tax on interest paid to a US lender. Interest for which the source State grants benefits of the Convention will be taken into account for tax purposes by a resident of the residence State. The protocol with Japan entered into force on August 30 2019 provides the following amendments to the 2003 tax treaty.

United States of America 0 1 10 0 2 0 2 1. For further information on tax treaties refer also to the Treasury Departments Tax Treaty Documents page. Explanation also provides that the regularly traded.

In an effort to strengthen the bilateral economic relationship and promote cross-border investment Japan and the US signed a protocol to amend the 2003 income tax treaty between the two countries on 25 January 2013. Explanations above are based on Japanese domestic tax law. If you have problems opening the pdf document or viewing pages download the latest version of Adobe Acrobat Reader.

Requirements to obtain exemption from withholding tax on dividends from subsidiaries will be relaxed as follows. US persons making payments withholding agents to foreign persons generally must withhold 30 of payments such as dividends interest and royalties made to foreign persons. The President signed it into law on August 6 2019.

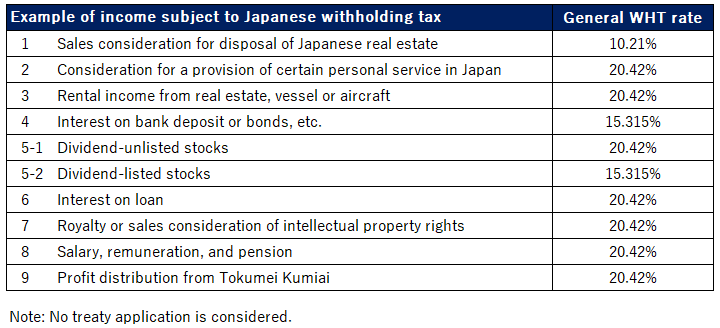

From United States tax to interest received by residents of Japan on debt obligations guaranteed or insured or indirectly financed by those Japanese banks or insured by the Government of Japan. Interest on bank deposits andor certain designated financial instruments is subject to a 15 national WHT and 5 local inhabitants WHT 20 combined. Real property interest also includes certain foreign corporations that have elected to be treated as US.

The complete texts of the following tax treaty documents are available in Adobe PDF format. The 2013 protocol introduces a number of changes to the treaty such as a general withholding tax exemption for interest a broader withholding tax. Holding company regime There is no holding company regime.

In an effort to strengthen the bilateral economic relationship and promote cross-border investment Japan and the US signed a protocol to amend the 2003 income tax treaty between the two countries on 25 January 2013. The US Japan tax treaty provides explicit rules to decide whether treaty benefits are available to an entity or its owners generally depending on eachs country of residence and which entity or owner has liability for taxes on the entitys income. 4 The term US.

Under US domestic tax laws a foreign person generally is subject to 30 US tax on a gross basis on certain types of US-source income. Source under the pre-amended tax treaty all interest will be exempt under the amended tax treaty in principle.

Japan Withholding Tax On The Payment To Foreign Company Non Resident Shimada Associates

Japan Tax Treaty International Tax Treaties Compliance Freeman Law

Changes To The Us Japan Tax Treaty International Tax Accountant

2

Us Expat Taxes For Americans Living In Japan Bright Tax

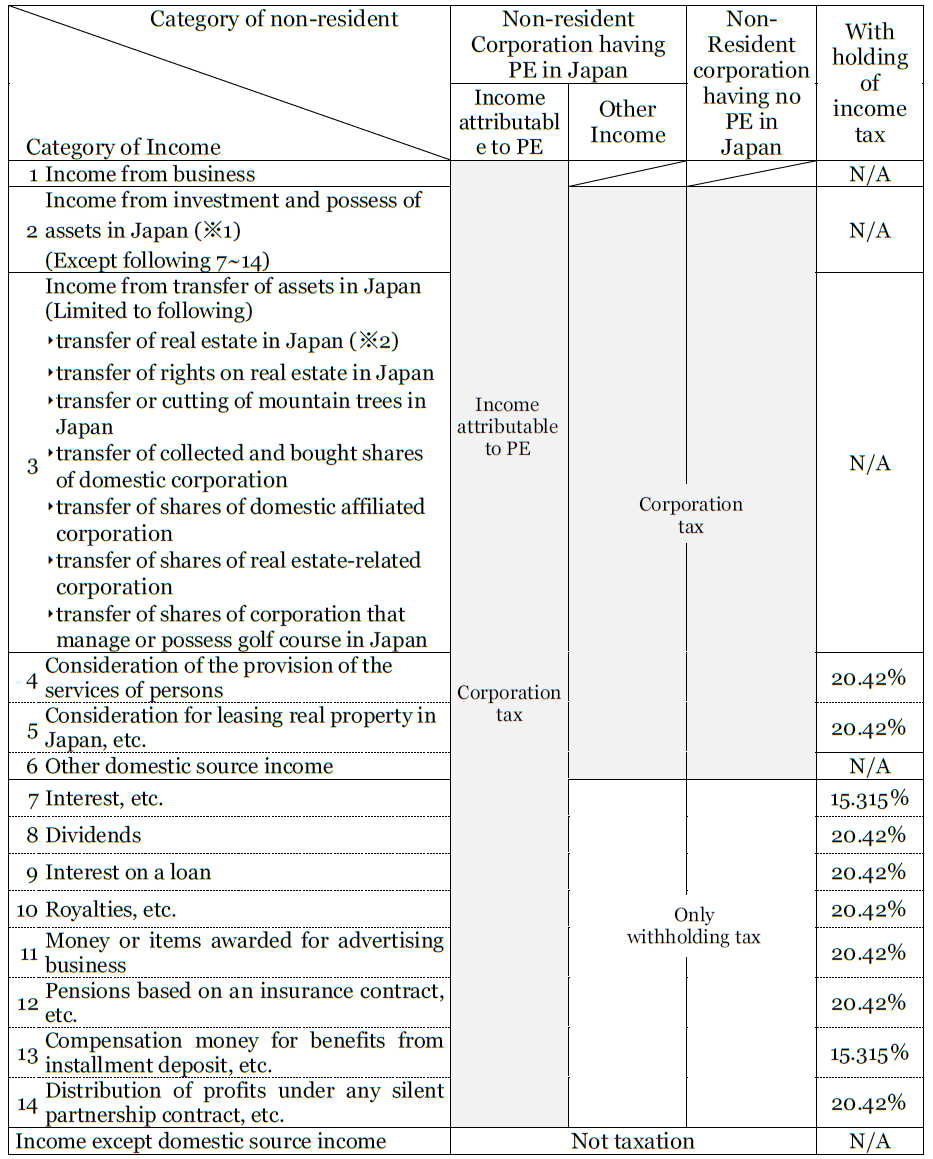

Japanese Withholding Tax Imposed On Non Resident Suga Professional Tax Services

Unraveling The United States Japan Income Tax Treaty And A Closer Look At Article 4 6 Of The Treaty Which Limits The Use Of Arbitrage Structures Sf Tax Counsel

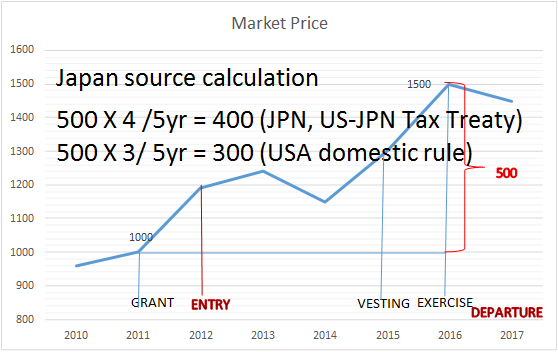

Income Tax On Stock Award For Expatriate Ata Tax Accountant Office

Us Expat Tax For Americans Living In Japan All You Need To Know